If you want to retire early, one of the biggest mistakes you can make is focusing only on your total net worth.

The better question is: how much of your money is actually accessible before age 59.5?

That is where a taxable brokerage account stops being a nice extra and starts becoming a real retirement tool. For many early retirees, it is the bridge account that funds life between the day work ends and the day retirement accounts become easier to access.

Use the calculator above — preset to a retire-at-50 scenario with $40K spending — to model your own bridge, then read the breakdown below to understand how the taxable brokerage number is calculated.

Quick Answer

There is no one-size-fits-all taxable brokerage target. The amount you need depends on five things:

- Your retirement age

- Your annual spending

- How many years you need to bridge before age 59.5

- Your healthcare costs before Medicare at 65

- Whether you have backup access from Roth contributions, Rule of 55, or Rule 72(t) / SEPP

A simple starting formula:

Taxable needed = (annual spending x bridge years) + healthcare costs + 15-25% buffer

The younger you retire, the larger that taxable bridge usually needs to be.

🧮 Calculate your exact gap: The Taxable Gap Calculator shows exactly how much accessible money your plan is missing for your specific retirement age, spending, and account mix.

Why Taxable Brokerage Matters Before 59.5

A lot of retirement content online focuses on "the number." Hit $1 million. Hit 25 times spending. Then retire.

That framing is incomplete.

Two people can each have the same portfolio value and have very different early retirement odds depending on where the money sits.

On paper both look equally wealthy. In real life Person A has a much cleaner bridge. That is why the taxable brokerage question matters so much.

The Taxable Bridge Formula

A useful first estimate:

Taxable needed = (annual spending x bridge years) + bridge healthcare costs + safety buffer

Where:

- Annual spending is what the portfolio needs to cover during the bridge

- Bridge years is the number of years until age 59.5

- Bridge healthcare costs is your out-of-pocket health coverage estimate before Medicare

- Safety buffer covers taxes, inflation, market drawdowns, and irregular expenses

For most households a 15% to 25% buffer is a reasonable starting point.

Example Estimates by Retirement Age

Here is a planning table using $40,000 annual spending and rough healthcare estimates of $12,000 per year before Medicare.

The most important takeaway: retirement age changes the taxable need dramatically. A person retiring at 50 usually needs a much larger flexible bucket than a person retiring at 57, even if their total portfolio is the same size.

Why Healthcare Changes the Number

This is where many early retirement plans get too optimistic.

If you retire before 65 and lose job-based health coverage, you will likely need Marketplace insurance until Medicare eligibility. A 50-year-old may need 15 years of non-Medicare coverage. A 55-year-old still needs 10 years.

Healthcare is part of the bridge. If you leave it out, your taxable brokerage target will probably be too low.

Example: Retiring at 50

You expect $40,000 annual spending and roughly 9.5 years until age 59.5.

Spending-only estimate: $40,000 x 9.5 = $380,000

Add healthcare and a buffer and your taxable brokerage target can easily move toward $450,000 to $600,000+ depending on your assumptions and backup access tools.

If you do not have enough taxable access, you need another bridge tool:

- Roth contributions — accessible at any age, tax-free and penalty-free

- Roth conversion ladder — requires 5-year seasoning, requires planning ahead

- Rule 72(t) / SEPP — works at any age, but locks you into fixed payments

- Part-time income — even $15,000-$20,000/year dramatically reduces bridge pressure

📊 Calculate your 72(t) payment: If taxable falls short, the SEPP Calculator shows your annual payment across all three IRS-approved methods — so you can see exactly how much of the gap 72(t) could close.

See the complete guide to Rule 72(t) / SEPP for how that exception path works.

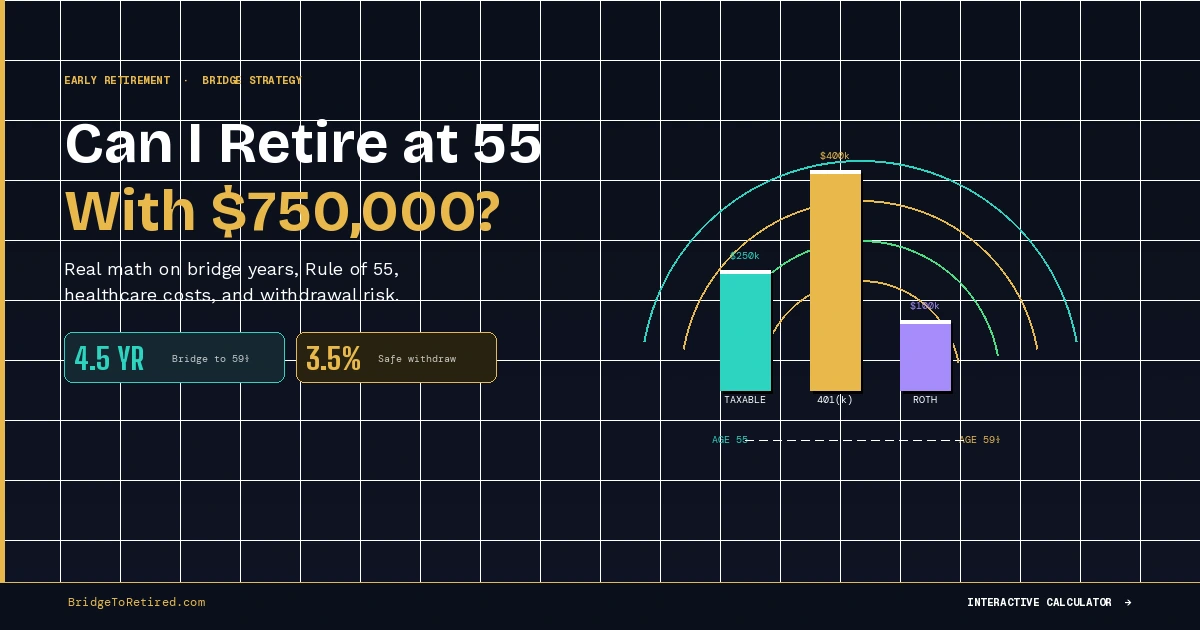

Example: Retiring at 55

Same annual spending: $40,000. But the bridge to 59.5 is only 4.5 years.

Spending bridge: $40,000 x 4.5 = $180,000

That is a completely different problem. And depending on the situation, Rule of 55 may also be relevant if you separate from service in or after the year you turn 55 and your employer plan supports distributions. That can reduce how much taxable brokerage is required — though it does not solve healthcare before Medicare.

A 55-year-old may be able to retire with a smaller taxable account if spending is moderate, Rule of 55 is available, and healthcare is manageable. See the full retire at 55 with $750,000 breakdown for a detailed scenario.

Run your own bridge numbers

The right taxable brokerage target depends on your specific spending, retirement age, healthcare costs, and which bridge tools apply to you. Use the calculator at the top of this page — or test more scenarios in the free Bridge Planner.

When Taxable Brokerage Does Not Need to Cover Everything

A taxable brokerage bridge account is often the cleanest bridge tool — but it does not always need to do all the work alone.

Common Mistakes

Treating taxable brokerage as extra — for traditional retirement at 65+ it may feel extra. For early retirement it is often core infrastructure.

Ignoring healthcare — healthcare before Medicare is one of the biggest reasons bridge math breaks. It belongs in the calculation. See the full health insurance before Medicare guide.

Counting on Rule of 55 too early — Rule of 55 is powerful in the right situation, but it generally does not solve a retire-at-50 plan.

Overestimating 72(t) flexibility — Rule 72(t) can help, but it creates rigidity. It is not the same as having liquid bridge cash.

Using the same bridge number for everyone — the taxable number for someone retiring at 57 is not the same as for someone retiring at 50. Age matters enormously.

Forgetting the buffer — car repairs, roof work, market drawdowns, and taxes do not stop just because your spreadsheet looked clean.

The Right Way to Think About This

The phrase that matters here is not just taxable brokerage. It is taxable brokerage bridge account.

That frames the account correctly. You are not just investing in a taxable account because you ran out of tax-advantaged space. You are building an access bucket — a bridge bucket — a flexibility bucket.

That bucket lets you:

- Delay tapping retirement accounts

- Keep the 401(k) compounding longer

- Avoid unnecessary penalty exposure

- Manage early-retirement years with less financial stress

This is the connective tissue between everything else in early retirement planning — the Roth conversion ladder, the 72(t) SEPP structure, the optimal withdrawal order, and the bridge strategy itself.

🎯 Grade your full plan: The Retirement Readiness Score scores your bridge across withdrawal rate, account access, healthcare, and sequence risk — and tells you exactly what needs to change before you retire.

Frequently Asked Questions

What is a taxable brokerage bridge account? A taxable investment account used to fund the years between early retirement and easier retirement-account access — typically before age 59.5.

Why do early retirees need taxable brokerage? Because retirement-account access is more limited before age 59.5. Taxable brokerage gives flexible access without automatically triggering the 10% additional tax on early distributions.

Does taxable brokerage need to cover the whole bridge? Not always. Roth contributions, Rule of 55, Rule 72(t), or part-time income may reduce how much taxable money you need.

How does healthcare affect the taxable brokerage target? Healthcare before Medicare can add $54,000 to $270,000+ to the bridge depending on retirement age, household size, and subsidy eligibility. It belongs in the calculation.

Is Rule of 55 enough to replace taxable brokerage? Usually not by itself. It may help people retiring at 55 or later but does not solve healthcare costs or help someone retiring at 50 or 52.

Is 72(t) a substitute for taxable brokerage? Sometimes it can help bridge the gap, but it comes with strict payment rules and less flexibility. Better viewed as a backup tool, not a first choice.

How much taxable brokerage do I need to retire at 50? At $40,000 annual spending, roughly $380,000 for spending alone across the 9.5-year bridge, plus healthcare and a buffer — often $450,000 to $600,000 depending on backup access tools.

How much taxable brokerage do I need to retire at 55? At $40,000 annual spending, roughly $180,000 for the 4.5-year spending bridge, plus healthcare. Rule of 55 may reduce the required taxable amount if it applies.

Related: What Is a Retirement Bridge Strategy? · The Taxable Brokerage Account: Your Secret Weapon · Rule 72(t) / SEPP Explained · Roth Conversion Ladder Guide · Health Insurance Before Medicare · Can I Retire at 55 With $750,000?