Can you retire at 55 with $750,000? The honest answer is: maybe — but the number alone isn't what decides it.

What actually decides it is how much of that $750,000 is accessible before 59½, how much you plan to spend each year, what healthcare will cost before Medicare, and how your portfolio holds up in the first few years after you stop working. Use the calculator above to model your specific situation before reading the breakdown below.

Why Age 55 Is Different From Every Other Early Retirement Age

Retiring at 55 creates a 4.5-year bridge before your 401(k) unlocks penalty-free at 59½. That gap is shorter than retiring at 50, but it still requires deliberate planning — and it comes with one major advantage most early retirement articles never mention.

The Rule of 55: The Bridge Tool Most People Miss

If you leave your employer in the calendar year you turn 55 or later, you may qualify for penalty-free withdrawals from that specific employer's 401(k) under what's known as the Rule of 55. No fixed payment schedule. No complicated SEPP calculations. Just direct access to your largest account starting at exactly 55.

Critical caveat: The Rule of 55 only works if you do not roll your current employer 401(k) into an IRA before retiring. If you roll it over, you lose this benefit permanently. Do not roll your active employer 401(k) into an IRA if you are planning to use Rule of 55 access.

If the Rule of 55 applies to you, it dramatically simplifies your bridge. Instead of relying entirely on taxable assets or setting up a 72(t) SEPP structure, you can draw from your largest account without penalty from day one.

The Account Location Problem

$750,000 structured two different ways produces two very different retirements at 55:

Same total portfolio. Very different early-retirement flexibility. Person B is not broke — but Person B has a structural problem that net worth alone doesn't reveal.

This is the core issue the bridge strategy addresses: retiring before 59½ isn't just a savings question, it's an account structure question.

🧮 Find your bridge gap: The Taxable Gap Calculator shows exactly how much accessible money your plan is missing — and what it would take to close it before retirement.

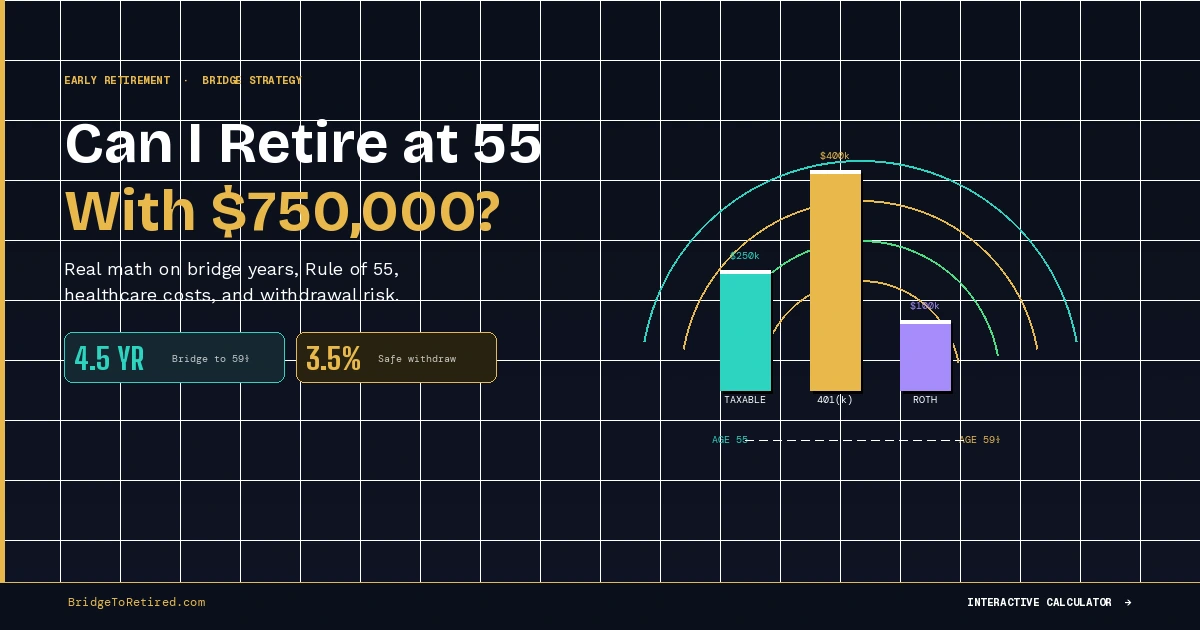

Example: When $750,000 at 55 Can Work

If you want to make this more concrete, here is a simple example.

Let's say your portfolio looks like this at age 55:

- Taxable brokerage: $250,000

- 401(k) / IRA: $400,000

- Roth: $100,000

- Total portfolio: $750,000

- Annual spending target: $35,000

In this example, your bridge period lasts about 4.5 years until age 59½.

If you fund most of those bridge years from taxable assets while leaving the 401(k) untouched, the tax-deferred account can continue compounding in the background. At a 6% annual return, $400,000 grows to roughly $520,000 by age 59½ if it stays invested.

That does not make the plan automatic or risk-free. You still need to account for healthcare costs, inflation, taxes, and poor early market returns. But this type of account mix is much more flexible than a portfolio where nearly all the money is locked inside a traditional 401(k).

The key point is simple: two people can both have $750,000, but the one with better account access usually has the better early-retirement plan.

That is why early retirement is not just about how much you have. It is about where the money sits and when you can use it.

A Simple Way to Think About $750,000

Before running detailed scenarios, a quick withdrawal rate screen gives you a starting range:

If your annual spending is around $30,000 or less, $750,000 at 55 starts to look workable. If your spending is $45,000 to $60,000+, the math gets hard without another income source, part-time work, or unusually low healthcare costs.

Three Scenarios: Does $750,000 Work at 55?

Scenario 1: Lean Retirement — Probably Workable

Setup: $750,000 total | $28,000/year spending | No debt | Meaningful taxable account or Rule of 55 access

At $28,000 per year, your 4.5-year bridge requires roughly $128,000 in accessible funds before 59½ — very manageable if you have a decent taxable brokerage, accessible Roth contributions, or Rule of 55 access to your 401(k).

The math works at the portfolio level too. $28,000 / $750,000 = 3.7% withdrawal rate — reasonable for a 35-year retirement horizon.

The risks are still real: a bad first few years in the market, higher-than-expected healthcare costs, or a major unplanned expense can strain a lean plan. But with flexibility and low fixed expenses, a lean retiree has genuine room to make this work.

Scenario 2: Middle-of-the-Road — Gray Zone

Setup: $750,000 total | $40,000/year spending | Marketplace health insurance | Normal home costs

At $40,000 per year, you're looking at a 5.3% withdrawal rate — above what most research supports for a 35-year retirement. This plan is not impossible, but it requires three things to go right simultaneously:

- Strong bridge assets (taxable brokerage, Roth contributions, or Rule of 55 access)

- Decent early market returns — a bad sequence in years 1-5 is the main risk

- Healthcare costs that stay manageable

This is where modeling matters most. A "feels like it should work" intuition about $750,000 at $40,000/year spending is not the same as running the numbers. See the calculator above.

Scenario 3: Higher Spending — Probably Not Enough

Setup: $750,000 total | $55,000+/year spending | Private health insurance | Lifestyle costs

At $55,000 per year, your withdrawal rate is 7.3% — too high for long-term portfolio survival without another income source. The bridge years require significant accessible capital, early market performance has enormous leverage on the outcome, and there is very little margin for unexpected costs.

At this spending level, $750,000 is probably not enough at 55 unless you have a pension, substantial part-time income, a spouse's income, or a plan to reduce spending in the first few years.

🧮 Test your exact numbers: Enter your balance, spending, account mix, and target retirement age into the Retirement Age Calculator to see whether your specific scenario holds up across different market and spending assumptions.

How Much Monthly Income Does $750,000 Provide at 55?

This is usually the first question people ask, so here is the honest range:

The 4% rule gives you roughly $2,500 per month before taxes and healthcare. That is the headline number many people focus on — but the real usable amount can drop fast once you add health insurance, taxes, and irregular expenses.

A more realistic net spending budget for someone retiring at 55 with $750,000 is $1,800–$2,200/month after healthcare — enough to cover modest housing, food, transportation, and basic lifestyle in a lower-cost area, but not enough for a high-cost city, frequent travel, or significant discretionary spending without additional income.

Is $750,000 Enough for a Married Couple to Retire at 55?

For most couples, $750,000 at 55 is tight — but not impossible under the right conditions.

The challenge is twofold: two people cost more than one, and healthcare before Medicare is the biggest wildcard. A couple with unsubsidized ACA coverage could easily spend $20,000–$30,000/year in premiums alone before out-of-pocket costs. That single line item can consume most of what a 3.5% withdrawal rate generates.

Where it can work for a couple:

- One spouse continues part-time work — even $15,000–$20,000/year dramatically reduces portfolio pressure in the early years

- Housing is owned outright or very low cost — eliminating a mortgage changes the monthly math significantly

- ACA subsidies apply — income-managed spending below 400% FPL can bring premiums to $6,000–$12,000/year for both

- Spending is genuinely lean — $35,000–$40,000/year total for two in a low-cost area is tight but doable

Where it typically doesn't work: two people with $45,000–$60,000+ in combined spending, unsubsidized healthcare, and no other income. At that level, $750,000 is a starting point, not a finish line.

Bottom line for couples: $750,000 at 55 is only reliably workable with low housing costs, at least one income source, or strong ACA subsidy planning — ideally all three.

Social Security: How It Changes the Math After 62

$750,000 has to work harder during the years before Social Security kicks in. Once it does, portfolio pressure drops significantly — which is why SS timing is one of the highest-leverage decisions in an early retirement plan.

For a $750,000 portfolio, the difference between claiming at 62 vs 70 can be $8,000–$15,000/year in additional lifetime income. That gap significantly affects how long your portfolio needs to last and how aggressively it needs to be drawn down.

The practical implication: if your portfolio can survive the bridge years and the pre-SS gap with reasonable withdrawals, delaying SS to 67 or 70 is usually the strongest long-term move. Model both scenarios before deciding.

The Real Make-or-Break Factors

Healthcare Before Medicare

Retiring at 55 means 10 years before Medicare eligibility at 65. ACA marketplace plans are available, but costs vary significantly based on your income level in retirement:

- With income-managed ACA subsidies (below 400% FPL): $6,000–$12,000/year in premiums

- Without subsidies: $15,000–$25,000+/year for a couple

- Out-of-pocket costs on top of premiums: $3,000–$9,000/year in normal health years, up to the OOP maximum in bad ones

Healthcare is the most commonly underestimated line item in early retirement planning. A conservative budget of $12,000–$18,000/year until 65 adds $120,000–$180,000 to your real funding requirement — before out-of-pocket maximums.

See Health Insurance Before Medicare: Your Options in Early Retirement for a full breakdown of ACA strategies, COBRA, and health share alternatives.

Sequence of Returns Risk

A rough first few years in the market can permanently damage a new retirement more than the same bad returns later. This is especially acute during the bridge years, when you are withdrawing from a portfolio that has no new contributions coming in.

The math is asymmetric: a 30% portfolio drop in year one of retirement plus ongoing withdrawals creates a much harder recovery than a 30% drop in year ten. Your bridge is the period of maximum exposure.

See Sequence of Returns Risk: The #1 Threat to Early Retirement for a detailed treatment of this risk and how to protect against it.

Too Much Money in Tax-Deferred Accounts

If most of your $750,000 is in a traditional 401(k) or IRA and you don't qualify for the Rule of 55, your retirement may look fine on paper but leave you income-poor during the bridge years without setting up a 72(t) SEPP structure.

Your bridge funding sources in order of simplicity:

- Taxable brokerage — cleanest option, no restrictions, capital gains rates

- Roth contributions (not earnings) — accessible at any age, tax-free and penalty-free

- Current employer 401(k) via Rule of 55 — penalty-free if you qualify, ordinary income tax applies

- Any account via 72(t) SEPP — works at any age on any account, but locks you into fixed payments for 5 years or until age 59.5

The taxable brokerage account is your most flexible bridge tool. If you have not built enough in taxable, assess whether Rule of 55 or 72(t) applies before concluding the plan doesn't work.

When $750,000 at 55 Is More Likely Enough

- Annual spending is $28,000–$35,000 or less

- You own your home or have very low housing costs

- You have meaningful taxable brokerage assets or qualify for Rule of 55

- You are flexible with spending if markets underperform early

- You plan to delay Social Security to 67 or 70

- You have a realistic healthcare cost estimate built into your budget

When $750,000 at 55 Is Probably Not Enough

- Annual spending is $45,000–$60,000+

- You carry significant debt

- Healthcare costs will be high and unsubsidized

- Nearly all savings are in tax-deferred accounts with no penalty-free access strategy

- You want zero flexibility and no backup income option

- You are retiring into a weak or declining market with no cash buffer

What to Model in the Calculator

Before making this decision, run these variations:

- Spending at $28,000, $35,000, and $40,000 — see how sensitive the outcome is to that one input

- Lower return assumptions (4% and 5% instead of 6%) — test the downside case

- Healthcare costs added to annual spending — most people forget this

- Different taxable / 401(k) / Roth splits — same total, different structure

- What happens if you retire at 56 or 57 instead — small delays can dramatically improve outcomes

- What happens if you work part-time for the first 2 years — reducing early withdrawals is one of the highest-leverage moves available

Frequently Asked Questions

Can I retire at 55 with $750,000 and no pension? Possibly, but it depends heavily on annual spending, healthcare costs, and whether enough of your money is accessible before 59½. Rule of 55 access or a strong taxable brokerage significantly improves the odds. Without either, you'll need to model a 72(t) SEPP structure.

Is $750,000 enough for a married couple to retire at 55? For most couples, it's tight. Low housing costs, lean spending ($28,000–$35,000/year total), and income-managed ACA subsidies make it more viable. Higher healthcare costs and two people's expenses make it harder. Model your specific numbers.

What if most of my $750,000 is in a 401(k)? That creates a bridge-year problem unless you qualify for the Rule of 55 (leaving your employer at age 55 or older) or are willing to set up a 72(t) SEPP structure. Without a penalty-free access strategy, a 401(k)-heavy portfolio leaves you income-poor during the bridge years even if your net worth looks fine on paper. Do not roll your current employer's 401(k) into an IRA if you plan to use Rule of 55.

What is the Rule of 55 and how is it different from Rule 72(t)? The Rule of 55 lets you withdraw from your current employer's 401(k) without the 10% penalty if you leave that job in the calendar year you turn 55 or later. It requires no fixed payment schedule and no IRS approval. Rule 72(t) is more flexible — it works on any account at any age — but locks you into substantially equal periodic payments (SEPP) for 5 years or until age 59.5, whichever is later. For someone retiring at exactly 55 with a large current-employer 401(k), Rule of 55 is usually simpler.

Should I use the 4% rule for this decision? Use it as a rough screening tool, not a final answer. The 4% rule was designed for 30-year retirements starting around 65. At 55 you may be planning a 35-year retirement — which brings the research-supported safe withdrawal rate down to roughly 3.3%–3.5%. Model your specific numbers rather than anchoring to 4%.

What if I have no taxable brokerage at all? This is one of the harder scenarios. Without taxable assets, you need either Rule of 55 access (if leaving a current employer at 55+) or a 72(t) SEPP structure to generate bridge income. Both are doable with planning but add complexity. Going forward, consider rebalancing contributions between your 401(k) and taxable brokerage to build accessible assets before your target retirement date.

How does Social Security factor into this? Social Security doesn't start until at least 62, and delaying to 67 or 70 substantially increases the lifetime benefit. For a $750,000 portfolio, a $24,000/year SS benefit starting at 67 meaningfully reduces portfolio pressure in your late 60s and beyond. Model your plan both with and without SS to understand your dependence on it.

The Bottom Line

Yes, you can potentially retire at 55 with $750,000 — but the better question is: what spending level and account mix make $750,000 work at 55?

The answer depends on four things: how much you spend, how your money is structured across taxable, 401(k), and Roth accounts, what healthcare will actually cost before 65, and whether you qualify for the Rule of 55. Get those four inputs right and $750,000 can work. Get them wrong and the same number fails — not because the portfolio is too small, but because the structure is wrong.

If you have modest expenses, enough accessible money for the 4.5-year gap to 59½, and a realistic healthcare budget, $750,000 is workable. If your spending is higher or most of your money is locked in the wrong accounts without a penalty-free access strategy, it probably isn't — yet.

The smartest next step is to model your specific numbers across spending levels, account mixes, and healthcare scenarios — not anchor to a headline balance. Use the Retirement Age Calculator to test your scenario, then download the free Bridge Planner to map exactly how your accounts need to be structured to get there.

🎯 Grade your plan before you retire: The Retirement Readiness Score scores your bridge across withdrawal rate, account access, healthcare, and sequence risk — and flags what needs to change before you pull the trigger.

Related: What Is a Retirement Bridge Strategy? · The Taxable Brokerage Account: Your Secret Weapon · Rule 72(t) / SEPP Explained · Health Insurance Before Medicare · Sequence of Returns Risk