If you want to retire at 50, the biggest challenge is usually not your total net worth. It is the gap between early retirement and standard retirement-account access.

That is what makes age 50 different. In general, distributions from qualified retirement accounts before age 59½ can trigger a 10% additional tax unless an exception applies. And the Rule of 55 generally helps only if you separate from service in or after the year you turn 55 — which means it does not solve the problem for someone retiring at 50.

So the real question is not just, "Can I retire at 50?" It is: how do I fund the years from 50 to 59½, which accounts should I use first, how do I handle health insurance before Medicare, and how do I avoid wrecking the plan with taxes or bad timing?

Quick Answer

You can retire at 50 if you have enough assets, controlled spending, and a clear retirement bridge strategy for the years before age 59½. For many people, the plan works best when it combines taxable savings, careful withdrawal sequencing, and — in some cases — either a Roth conversion ladder or a 72(t) / SEPP strategy. Medicare generally starts at 65, so healthcare planning matters more than most early retirees expect.

Why Retiring at 50 Is Harder Than Retiring at 55

Age 55 gets a lot of attention because of the Rule of 55 exception. But for someone retiring at 50, that exception is not available. That means you are dealing with:

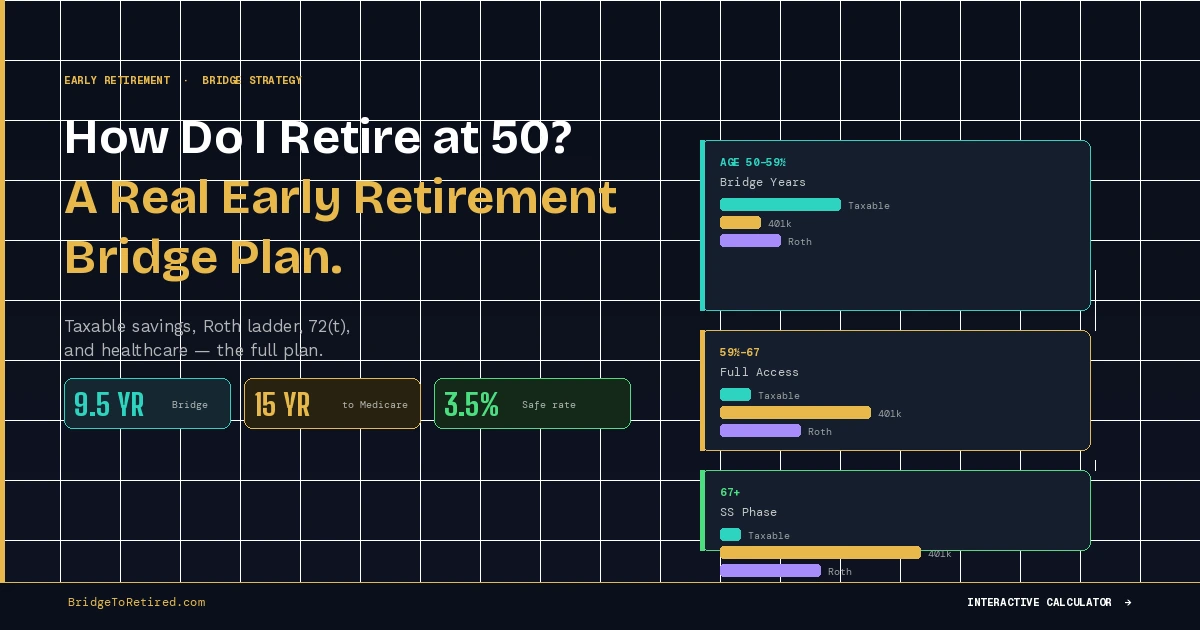

- A roughly 9.5-year bridge until age 59½

- A 15-year gap until Medicare

- Potentially an even longer wait until Social Security begins

That is a much bigger planning problem than simply hitting a certain portfolio number.

🧮 Find your earliest viable retirement age: The Retirement Age Calculator shows whether your current balance, spending, and account mix support retiring at 50 — or whether 52, 54, or 55 is more realistic.

The 9.5-Year Bridge Problem

This is the heart of the issue.

If you retire at 50, your portfolio has to do two jobs at once: fund your current lifestyle, and preserve enough long-term money for later decades. That is why early retirees need a real bridge strategy, not just a savings target. Without a bridge plan, "retire at 50" can turn into "retire at 50 and scramble at 53."

What Money Can You Use First?

In most cases, the cleanest early-retirement bridge starts with taxable assets. The taxable brokerage account is so powerful for early retirement precisely because it gives you flexibility without automatically triggering the 10% additional tax that can apply to early retirement-account distributions.

If taxable assets are not enough, some retirees look at Roth assets, some plan a Roth conversion ladder, and some consider substantially equal periodic payments under Rule 72(t). The IRS treats 72(t) as a real exception path, but it comes with strict rules and little room for improvisation.

The right answer depends on your account mix, taxes, spending, and how long the bridge has to last.

🧮 See your bridge gap: The Taxable Gap Calculator shows exactly how much accessible money your plan is missing for the 50-to-59½ gap — and what it would take to close it.

Example: When a Retire-at-50 Plan Starts to Look Real

Let's say your portfolio looks like this at age 50:

- Taxable brokerage: $300,000

- 401(k) / IRA: $500,000

- Roth: $150,000

- Total portfolio: $950,000

- Annual spending target: $42,000

This is not automatic success. But it is a real planning starting point.

The taxable bucket can cover a meaningful share of the 50-to-59½ bridge while the 401(k) continues compounding in the background. At 6% return, $500,000 grows to approximately $870,000 by age 59½ if left untouched. The Roth bucket adds flexibility if markets are weak or taxes need to be managed carefully.

That is a much better setup than a person with the same total net worth but nearly everything locked inside a traditional 401(k).

The key point is simple: at age 50, account access matters almost as much as net worth.

Three Workable Paths to Retire at 50

Path 1: The Taxable-Heavy Path

This is usually the simplest path. If you have a large enough taxable brokerage account, you can draw from it during the bridge years while leaving tax-deferred accounts mostly untouched. That gives your 401(k) and IRA more time to grow and keeps the plan flexible.

This path usually works best when your taxable balance is strong, your spending is moderate, your debt is low, and you do not need to force early retirement-account withdrawals. For many people, this is the cleanest and most resilient option.

Path 2: The Roth Conversion Ladder Path

A Roth conversion ladder can be a powerful long-term strategy for early retirees. The idea is to convert money from traditional retirement accounts to Roth over time and draw from those conversions later under the applicable rules.

This path is attractive because it can improve long-term tax control and create another source of accessible money. But it requires planning, patience, and tax awareness. It is not a same-day fix for someone retiring tomorrow.

Path 3: The 72(t) / SEPP Path

Under Section 72(t), there is generally a 10% additional tax on retirement-plan distributions taken before age 59½. One exception is a series of substantially equal periodic payments — often called 72(t) or SEPP. These payments must follow strict IRS rules, and changing the payment schedule improperly can trigger serious problems.

This path can help someone retire at 50, but it is not flexible. 72(t) is usually better viewed as a tool of necessity, not the dream option. It can work, but it should be modeled carefully before you commit.

Run your own numbers

A retire-at-50 plan depends on spending, account mix, bridge length, and healthcare. Test your scenario now — free, no account required.

Healthcare Before Medicare

This is one of the biggest reasons a retire-at-50 plan fails in real life.

If you retire at 50 and lose job-based coverage, you can buy Marketplace coverage — and losing that job-based coverage can qualify you for a Special Enrollment Period. But Medicare generally begins at 65 for most people, which means retiring at 50 creates a 15-year healthcare funding gap that has to be planned from day one.

See Health Insurance Before Medicare: Your Options in Early Retirement for a full breakdown of ACA strategies, COBRA, and health share alternatives.

Key ranges to plan around:

- With ACA subsidies (below 400% FPL): $6,000–$12,000/year in premiums

- Without subsidies: $15,000–$25,000+/year for a couple

- Out-of-pocket costs on top of premiums: $3,000–$9,000/year in normal health years

A retire-at-50 plan that ignores healthcare is not a plan.

What Can Go Wrong?

Even if the numbers look good on paper, several things can still break the plan:

Too Much Money in the Wrong Account — A portfolio can look healthy but still be hard to use if nearly everything sits in a traditional 401(k) or IRA with no penalty-free access strategy.

Underestimating Healthcare — A 15-year gap before Medicare can create far more pressure than people expect, especially if ACA subsidies are reduced or eliminated.

Sequence of Returns Risk — Bad early market returns matter more when withdrawals begin immediately after retirement. Your bridge years are the period of maximum exposure. See Sequence of Returns Risk for how to protect against it.

Spending Drift — Many people underestimate travel, home repairs, insurance, taxes, and family support costs in early retirement.

No Backup Flexibility — A plan is much safer when you can reduce spending, earn part-time income, or delay certain goals if markets underperform.

When Retiring at 50 Is Realistic

Retiring at 50 becomes much more realistic when:

- Your spending is controlled and you know the real number

- You have a meaningful taxable bridge bucket

- You understand how Roth and traditional assets fit together

- You have a realistic healthcare plan from day one

- You are willing to adapt if markets are weak in the early years

It also becomes more realistic when you stop asking only "What number do I need?" and start asking "What withdrawal path will actually work?"

When It Is Probably Too Early

Retiring at 50 is usually too aggressive when:

- Most of your money is locked in tax-deferred accounts with no access strategy

- You still carry meaningful debt

- You have no healthcare plan

- Your spending is high and inflexible

- The whole plan depends on perfect market returns

Early retirement does not need perfection. But it does need margin.

How Much Do You Need to Retire at 50?

There is no single answer, but here is a useful range based on withdrawal rate research:

The 4% rule was designed for 30-year retirements. At age 50 you may be planning a 40-year retirement — which pushes the research-supported safe rate closer to 3.0%–3.5%. Model your specific numbers rather than anchoring to 4%.

🎯 Score your retire-at-50 plan: The Retirement Readiness Score grades your plan across withdrawal rate, account access, healthcare, and sequence risk — and tells you which flags are red before you pull the trigger.

Frequently Asked Questions

Can I retire at 50 without a pension? Yes, but usually only if you have enough assets, moderate spending, and a solid bridge strategy for the years before age 59½. Rule of 55 is generally not available at 50, so taxable savings, a Roth ladder, or 72(t) become the key tools.

Does Rule of 55 help if I retire at 50? Usually no. Rule of 55 generally applies when you separate from service in or after the year you turn 55. Retiring at 50 means you need a different bridge strategy for the first 9.5 years.

What is the biggest challenge with retiring at 50? For most people, it is funding the 9.5-year bridge before standard retirement-account access and the 15-year gap before Medicare. The math can work — but account structure and healthcare planning are what make or break it.

Should I use taxable brokerage first in early retirement? Often yes. Taxable assets are usually the most flexible option for bridge spending. They do not carry the early-withdrawal restrictions that traditional retirement accounts do, and long-term capital gains rates are typically lower than ordinary income rates.

Can 72(t) help me retire at 50? It can. 72(t) / SEPP is a legitimate IRS exception that allows penalty-free withdrawals from retirement accounts before 59½ if you follow a strict schedule of substantially equal periodic payments. The trade-off is inflexibility — once started, the schedule is hard to change without triggering penalties.

Can I use the Marketplace for health insurance if I retire at 50? Yes. If you retire before 65 and lose job-based coverage, you can buy Marketplace coverage, and that loss of coverage qualifies you for a Special Enrollment Period. Whether you qualify for subsidies depends on your income level in retirement.

The Bottom Line

If you want to retire at 50, the answer is not just "save more."

The real answer is to build a bridge. That means knowing what money is accessible first, how to fund the 50-to-59½ gap, how healthcare fits in before Medicare, and whether taxable assets, a Roth conversion ladder, or 72(t) make the most sense for your setup.

A better question than "Can I retire at 50?" is: what account mix and bridge strategy make retiring at 50 actually work?

The smartest next step is to model your specific numbers — not anchor to a headline portfolio size. Use the calculator above to test your scenario, then download the free Bridge Planner to map exactly how your accounts need to be structured to get there.

Related: What Is a Retirement Bridge Strategy? · The Taxable Brokerage Account: Your Secret Weapon · Rule 72(t) / SEPP Explained · Roth Conversion Ladder Guide · Health Insurance Before Medicare · Sequence of Returns Risk